Articles

May 7, 2025

What a U-Shaped Yield Curve Means for Corporate Debt Issuers

# Capital Markets

# Risk Management

NeuGroup Video: Chatham Financial’s Reuben Daniels on the current curve and how investors view duration risk.

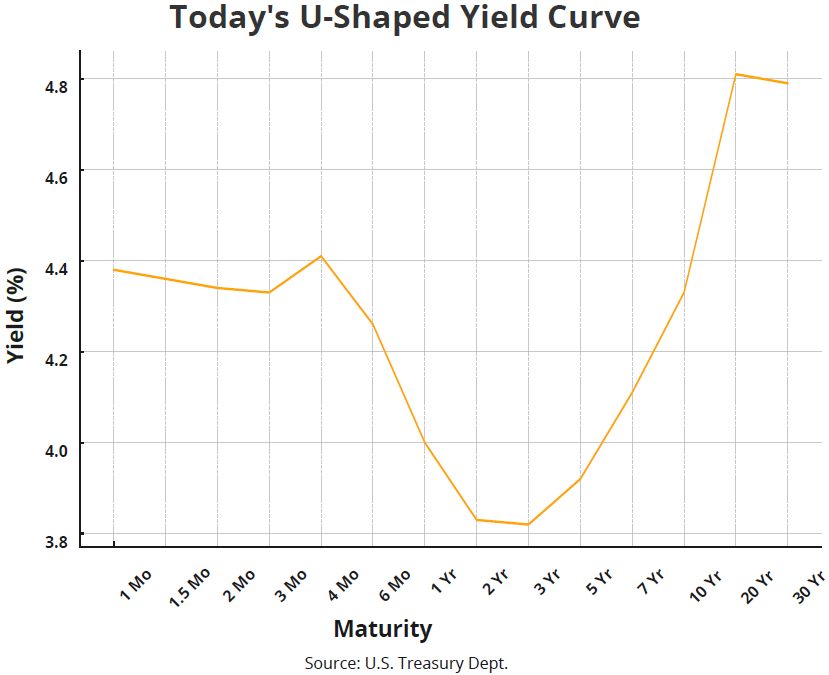

What does a U.S. Treasury yield curve that is neither steep nor inverted but looks something like the letter “u” mean for corporations that want to issue debt? Specifically, what does the u-shaped curve say about the appetite for risk and duration of fixed-income investors amid so much uncertainty about the economy, inflation and the Fed?

- Those are among the questions addressed by Reuben Daniels, head of investment banking at Chatham Financial, in a video you can watch by hitting the play button below. NeuGroup Insights recorded the video at the spring peer group meeting of NeuGroup for Mega-Cap Assistant Treasurers sponsored by Chatham.

A standoff and the belly of the curve. Mr. Daniels believes many of the points made in the video are even more relevant today given the deepening of the “u” in the last month or so. The shape, he said at the meeting, speaks to “a standoff between policymakers and the market,” meaning the Federal Reserve’s monetary policy and the outlook of bond market investors.

- “I think what we’re going to see over the next three months is one side or the other is going to prevail,” he says in the video. “That’s either going to be the Fed reducing rates and creating a steep yield curve by [lowering] short-term rates, or we’re going to see a capitulation by the market and we’re going to see the whole yield curve shift upwards in the long end.”

- At the March meeting, he said a key takeaway for issuers was the irony that investors were focused on “the belly of the curve,” between one- and three-year Treasuries, where rates are lower than both the short end (one-to-six months) and longer-term securities like 10-year Treasuries.

Reading investor order books. Recent corporate bond deals reveal mixed views among investors. “When we look at recent order books,” Mr. Daniels said at the meeting, “what we’re seeing is investors making a position that is, ‘I want to be in fives and not in 10s or I want to be in 10’s and not in fives,’ and taking a view on how they want to invest in that yield curve shape.”

- One assistant treasurer at the peer group meeting whose company did a bond deal this year said two-, three- and 10-year securities “flew off the shelf,” with weaker demand for five- and seven-year notes. Demand was strong, he added, for floating-rate notes.

- This week, Mr. Daniels said, “The ‘u’ has become more pronounced and so more investors are moving out to 10 years because they are getting paid for it.”

- For issuers, he said during the meeting, “The floating cost of capital is still high and perhaps one would want to bet on the fact that the Fed is going to capitulate and rates will fall and benefit from that decline in rates.

- “But the reality right now from a company perspective is one can extend maturity and still reduce cost. That’s a very unique position in the market and very beneficial to borrow longer term rather than shorter term.”

Dive in