Articles

January 28, 2026

How To Invest Cash in Emerging Market Debt—If It’s Right for You

# Investment Management

# Risk Management

A NeuGroup member and PGIM’s head of EM Debt on boosting yields and diversifying while managing risk.

Investing cash in emerging market (EM) debt will never make sense for treasury teams that for operational or risk tolerance reasons need complete liquidity and/or have no stomach for large drawdowns. But for others, allocating a small portion of cash not needed for core liquidity buckets can—if done properly—boost yields and diversify portfolios. If those outcomes sound good to you, read on!

- Members of NeuGroup for Cash Investments got a crash course in EM debt investing from two experts at the group’s fall meeting sponsored by PGIM Fixed Income. Managing Director Cathy Hepworth, PGIM’s Head of Emerging Markets Debt, presented with a client and NeuGroup member with deep knowledge of EM debt who plays a very active role in overseeing his company’s EM separately managed accounts (SMAs).

Step 1: Determine if EM is right for you. EM debt is most appropriate for companies with large amounts of liquid assets and excess cash that are managing portfolios for total return, the member said. “Some folks don’t have as much capital or cash,” he acknowledged. “And if you need the cash, you need the cash. If you’ve got the treasurer sitting there going, ‘I might need it tomorrow,’ then you’ve got to be in a money fund, or a bank deposit. It just can’t be in EM.”

- If you have the cash, to move forward you need to thoroughly understand the risk tolerance of senior leaders, he said. “Once you kind of figure out what you think that is, then you start saying, well, ‘How do I build a portfolio that’s going to maximize the return per unit of risk, the risk tolerance they give us?’”

- His team does it using an efficient frontier model. “We break our portfolio into different mandates,” he explained. “We have portfolios that are there for liquidity, portfolios or mandates for safety; we have portfolios that are there for yield enhancement; and then we have our income portfolios, which EM falls into.”

- “You’ve got to be comfortable with the asset class and what benefits it provides, and then how it fits in the portfolio context,” he added. He invests in both EM sovereigns and corporates.

- EM is right for his company for two main reasons. “We see a lot of advantages to it because one, it’s higher yielding; and two, it tends to react differently than Treasuries that we have in the portfolio or the [investment grade debt] we have, or even sometimes high yield, that don’t always move together. And so it provides diversification.”

Step 2: Know what you’re getting into. Be aware that the risks to EM debt include large drawdowns in specific countries (e.g., Argentina). “When EM goes down, it goes down,” the NeuGroup member said. “It’s not a 10% drawdown—it’s a 30% drawdown.” But with some distinct exceptions, “it bounces back. You have to live through it,” he added.

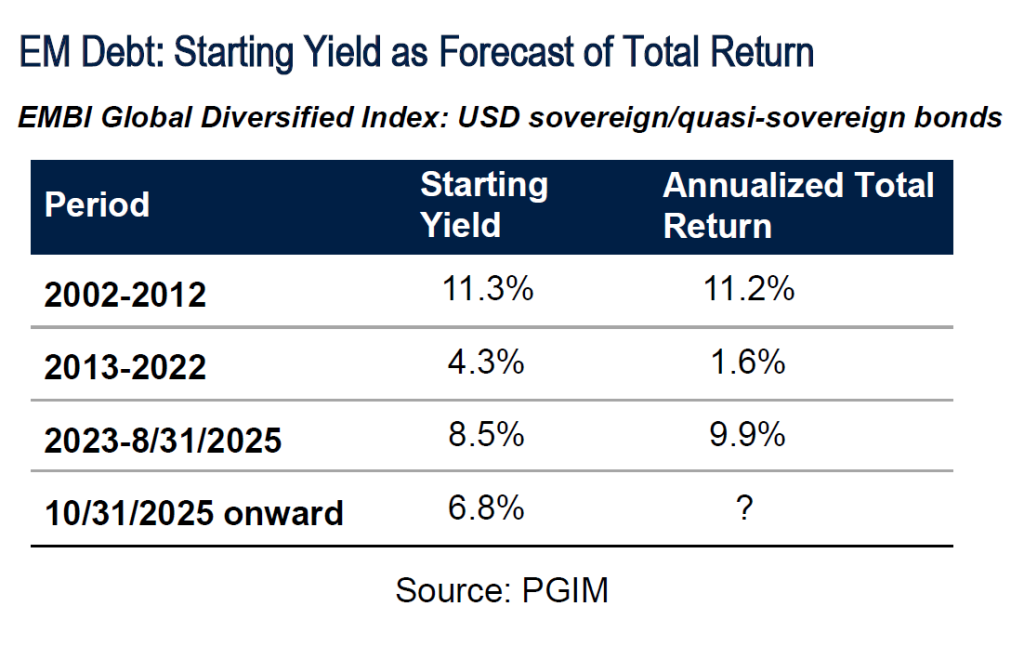

- PGIM showed charts demonstrating the long-term strength and moderate volatility of EM debt markets as measured by the EMBI Global Diversified index. The chart above shows starting yield as a predictor of total return over long periods. The 11.2% annualized total return between 2002 to 2012 includes a 12% decline in the index in 2008 during the global financial crisis.

- “The thing about EM is the bounce-back period because it’s a higher yielding asset class and it throws off these cash flows,” Ms. Hepworth said. “And so yes, it does have big drawdowns, but it comes back really quickly.”

- That said, you have to size the allocation to EM debt with the risks in mind—meaning it’s likely to be a relatively small part of the portfolio. The NeuGroup member, guided by the efficient frontier model and the comfort level of senior leadership, has about 5% in the asset class.

- “You keep a core amount in there,” he said. “And when it gets really cheap, maybe you lean into it a little bit. And when it gets a little expensive, maybe you take a little off the table.”

- To remove the risk that volatility in foreign exchange rates affects returns, the NeuGroup member now invests only in so-called hard currency EM debt that is denominated in U.S. dollars. “We used to have both local and hard currency; I just never liked being exposed to the local. It just didn’t give us the same kind of diversification benefits that I wanted.”

- Hedging the FX risk to invest in EM debt is an option but not for this member: “We have a whole group that runs FX that has billions of dollars of risk that we don’t need to add to in any way, shape, or form.” Ms. Hepworth advised that new investors to the asset class begin with hard currency EM debt.

Step 3: Find the right asset managers. The NeuGroup member’s internal team invests in many asset classes directly. But “some of the harder asset classes like this, we don’t manage any in-house,” he said. One key is finding SMA managers with access to finance ministers and other officials whose insights can inform investment decisions. “If your manager doesn’t have access to that type of breadth and quality of conversations, you probably need to find another manager.”

- Ms. Hepworth’s team has about 25 professionals covering emerging markets, including dedicated economists who are on the road in Asia, Latin American and Africa about 50% of the time. She emphasized the importance of the team’s understanding of qualitative factors in addition to monthly or quarterly data.

- “One of the reasons why EM trades the way it does is not so much because of the numbers. You have to get your arms around political risk. You have to get your arms around policy risk,” she said.

- “Oftentimes, there’s an inconsistency between fiscal policy and monetary policy and exchange rate policy. And often, there’s structural imbalances. So it’s those qualitative factors that I think are much more nuanced and much more of the art than the science part.”

- She said it’s imperative they understand how portfolio managers make decisions, and that their process and risk management tools are key. “How do they decide how they’re going to size those positions? How do they think about the different risks that are in the market? How do they do their analysis to understand country risk or to understand corporate risk?”

Step 4: Managing the investment managers. Unlike some SMA investors, the NeuGroup manager and his team closely monitor their EM portfolio, evaluating credit risk. “We have all kinds of ways to get to the bottom of things. And then we have a watch list and we have actions that we take against those particular names” to reduce positions, he said.

- “We have a weekly meeting with our treasurer and our head of capital markets where we talk through that watch list and talk about what we like, what we don’t like. So it’s very important to make sure we get credit right. Whether you call it micromanage, being helpful, or maybe not helpful, we’re probably a pain,” he said.

- For Ms. Hepworth, “EM lends itself to customizing what it is that the EM client wants.” That includes country exclusions, rating caps, duration limits and benchmark customization.

- The NeuGroup member noted that such restrictions complicate benchmarking—but are non-negotiable in practice. Ms. Hepworth added that you “can customize the benchmark to exclude single B’s, triple C’s, or anything that’s in default.”

Dive in

Related

Article

A “Perfect Storm” in Emerging Markets Shatters Hope for Some Investors

Jun 16th, 2020 • Views 9

Article

A “Perfect Storm” in Emerging Markets Shatters Hope for Some Investors

Jun 16th, 2020 • Views 9