Articles

July 15, 2026

Balancing Act: FX Hedging Runs on Rules, Judgment, Relationships

# Foreign Exchange

# Banking

A NeuGroup survey sponsored by U.S. Bank explores the push and pull between FX policy and discretion—and a similar tension at execution, where price competes with banking relationships.

Treasury teams rarely hedge FX by rigid formula or pure instinct—most operate somewhere in between, with policies that leave room for taking a view. A new survey conducted by NeuGroup Peer Research sponsored by U.S. Bank found another balance being struck in how members pick banking counterparties: The best price usually wins the trade, but relationships usually decide which banks get to bid. At a recent session of NeuGroup for Foreign Exchange, head of research Joseph Bertran presented the results and members compared how their programs handle both.

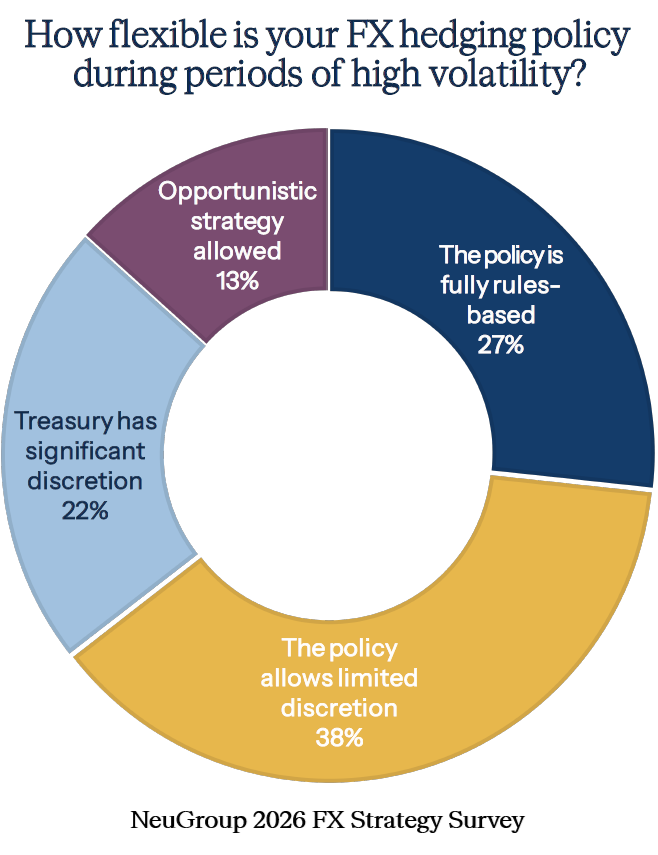

- While 73% of policies build in some flexibility, the day-to-day hedging decisions of most respondents are largely rules-based. Limited discretion is the most common setup (see chart below): a defined range around a target hedge ratio, or a strict hedge policy baseline with opportunistic action reserved for when the market trades at levels the team considers attractive.

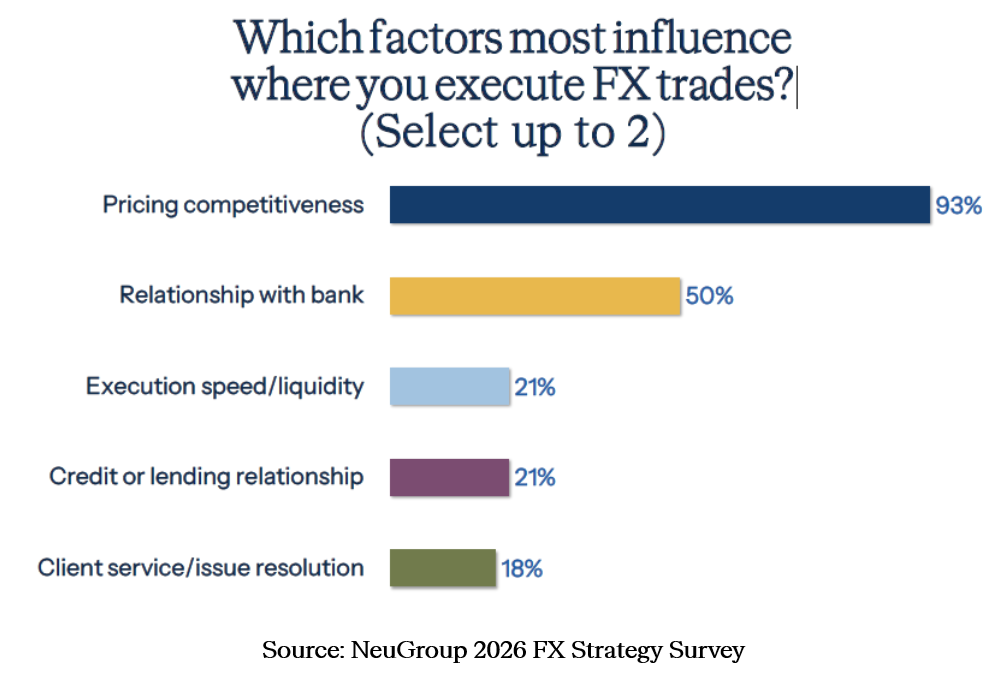

- Picking a counterparty involves its own tug-of-war: Pricing competitiveness is by far the biggest factor in determining where members execute FX trades, cited by nearly all respondents—but most also weigh the relationship, particularly if a bank is part of the company's revolver.

Rules vs. discretion. Most members who use discretion keep it modest. One runs a monthly program that layers hedges into a narrow band, covering 70% to 80% of a forecasted exposure and adding roughly 15 more percentage points as the underlying exposure date approaches; the judgment is choosing the higher or lower end of the band, which shifts the notional amount hedged by about 5% to 7%. The member said the goal is to "take as much emotion out of it" as possible.

- Another member described a “mechanical” baseline program the team uses by default, with opportunistic action reserved for significant market entry points the team has already judged attractive. When the euro recently hit a favorable exchange rate, they "took a lot of action," locking in P&L protection rather than waiting to see if the move extended.

- At the far end of the spectrum—where the survey found just 13% of members—one company runs a fully discretionary program, staffed by a dedicated team of traders that follows the markets closely and can hedge anywhere from 0% to 100% of an exposure based on their view of a currency.

- That member had a summer intern backtest the program against dollar-cost averaging: If the company had mechanically hedged a certain target of its forecast every month for a year, how would it have done? "Using a little bit of strategy, the numbers work out in our favor in every scenario," she said.

Price vs. relationship. Pricing competitiveness towers over every other factor in determining where members execute FX trades, cited by 93% of respondents; relationship with the bank ranks a distant second (see chart above). Members trade with enough banks to keep them honest: 80% say they spread FX trading across seven or more banks. But this is another scenario where FX managers must exercise discretion—relationships predominantly determine who gets asked to quote before the race even begins.

- U.S. Bank’s Charles Val, a co-presenter in the session, noted that pricing based on head-to-head competition can be hard to achieve for less liquid currencies. For example, members may struggle to line up enough dealers who can price a three-month Vietnamese dong trade in time to satisfy a requirement for competitive bidding.

- The revolver is where relationship judgment concentrates: 71% of members factor a bank's participation in the company's revolving credit facility into FX allocation at least sometimes, and 42% call the two strongly linked. In a live poll during the session, most members said they don't trade with banks outside their revolver at all.

- One member said it can also run the other direction: A bank that is angling to join the credit facility is first invited by the corporate to show how it performs on a few FX trades.

- Revolver relationships are also becoming more important for banks bidding on FX trades, Mr. Val said. As competition over pricing intensifies, clients' trading business is worth winning partly for the broader relationship it builds. "Banks prioritize two-way relationships where we can lean in on price to satisfy the competitive nature of the business, but also serve as trusted partners and advisors for sensitive transactions," he said.

Dive in