Articles

July 9, 2025

A Case for Offering Lifetime Income Options in 401(k) Plans

# Retirement Benefits

# People and Talent

Why defined contribution plan sponsors may want to provide retirees guaranteed income via solutions with annuities.

Insufficient savings for retirement is not the only problem facing millions of Americans whose working days have ended or will soon. For some retirees without pensions, the fear of outliving the assets they accumulate in defined contribution (DC) plans like a 401(k) prevents them from getting maximum satisfaction out of life after they leave the workforce.

- That, in broad strokes, is one argument for DC plan sponsors to consider offering participants retirement lifetime income options that often consist of annuities within target date funds. They allow the sponsor to provide the retiree with some guaranteed income—in some cases after their 401(k) has been depleted. Some proponents think of it as insurance that provides peace of mind at a price, here in the form of fees.

- Members of NeuGroup for DC and Financial Benefits attending their spring meeting learned about demographic, macroeconomic and behavioral issues driving lifetime income options as well as some of the details of one such offering by J.P. Morgan Asset Management (host of the meeting) and Prudential Financial (the meeting sponsor).

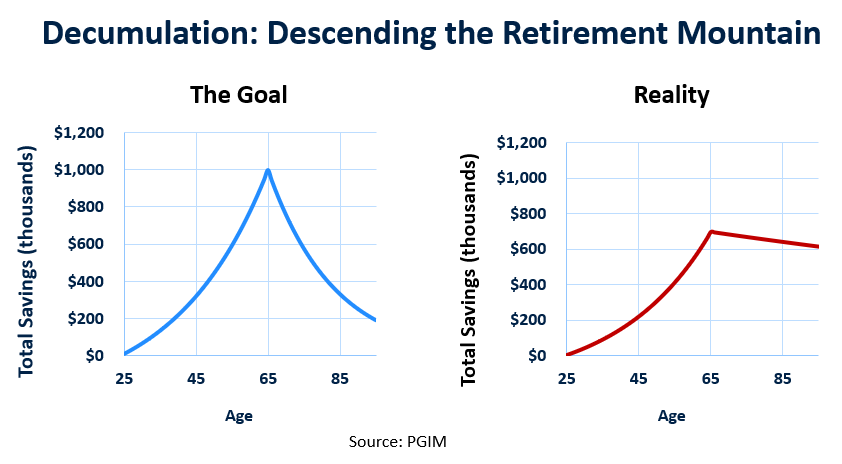

A decumulation dilemma. Prudential’s David Blanchett, head of retirement solutions at PGIM DC Solutions, showed charts (above) illustrating the so-called decumulation issue, both the goal and reality. The goal: workers accumulate assets as they climb the “retirement mountain;” they retire, descend from the peak and decumulate, spending at a steady clip for the rest of their lives. The reality, though, is the descent barely slopes because people hold on to savings.

- “Those that save don’t decumulate,” Mr. Blanchett said. While the desire to leave money to heirs is one reason, a lot of reluctance to spend is based on fear of outliving savings. “We’re seeing more people living longer, and that creates fear. The more fear people have in terms of market returns and the length of retirement, the less comfortable they are spending. People are afraid in retirement, not willing to enjoy what they’ve accumulated.”

Rethinking solutions. The belief that a goal of “saving is to do so in a way that we can maximize our happiness across our lifetimes,” leads Mr. Blanchett and other retirement experts to conclude that offering some form of guaranteed, lifetime income—like that provided by defined benefit pension plans—represents one way for DC plans to achieve that goal.

- In a separate session at the meeting, executives from Prudential and J. P. Morgan Asset Management discussed DC solutions that do that, including one that the two companies are now marketing to plan sponsors called SmartRetirement Lifetime Income. It offers a target-date fund and has an annuity option that pays guaranteed income if certain conditions are met, including the participant making only guaranteed minimum withdrawals.

- The solution, Mr. Blanchett said, “reflects an intelligent balance of the factors that need to be considered for these things to happen in the real world,” specifically “different behavioral, economic, and product realities/preferences that exist in the market.”

- It’s one of several products offering lifetime income through annuities embedded in target-date funds for DC plan sponsors to consider, including BlackRock’s LifePath Paycheck solution which “provides plan participants with the option to access guaranteed income as early as age 59 ½ by purchasing annuity contracts issued by Equitable and Brighthouse Financial,” according to a press release.

- Mr. Blanchett said, “Overall, I’m far less concerned about the specific form people and plan sponsors use; the key is creating products that plan sponsors are willing to adopt (that’s step one) and then participants are willing to utilize (that’s step two).”

A plan sponsor hurdle. While some companies have started offering retirement lifetime income options, many DC plan sponsors are just starting the process of understanding the solutions and evaluating the costs and benefits for workers and retirees. Legal risks for the sponsors are a concern given the proliferation of lawsuits filed by participants.

- That’s one reason some NeuGroup members responsible for DC plans who see a need for guaranteed income say they need more information before recommending solutions to investment committees. One benefits director contrasted the challenge of comparing fees for somewhat complex retirement income solutions that include annuities with the expense ratios of straightforward, passive index mutual funds.

- “I don’t know from a committee perspective that it’s quite so easy to compare the cost or the fees of this to be comfortable that you’re not going get sued,” he said. “I hate to boil it down to that, but you need to feel confident that what you’re offering is providing fair value for the cost that employees are paying. I think that’s a big hurdle.”

Portability and communication. Another key consideration for this member is the ability of workers to bring retirement income solutions with them when they change jobs. “We know that a good portion of our people leave before they’re retirement eligible, so I think portability is really important,” he said.

- It’s also critical, he added, that plan sponsors are able to explain and communicate clearly to participants how the solutions work in order to “drive utilization.” Participants must truly understand the benefits, costs and tradeoffs of giving up control of a certain portion of their portfolio if they opt to annuitize it.

The plan sponsor’s philosophy. Offering retirement income solutions may run counter to the desire of some companies to have DC participants leave their plans when they are no longer employed, a point acknowledged by Prudential’s Mr. Blanchett. “Plans have very different perspectives on how they how they want to engage their employees when they retire,” he said. “Some are adamant that they leave the plan. Some want to solve retirement for them.

- “You might want to kick them out the day that they retire, but you should still be doing things 10 years up until then to help them get there,” he added. “Or even if they don’t retire in your plan, you still want them to retire, right? And therefore doing things to help them get there I think is really, really important.”

- A benefits manager at the meeting said his company’s philosophy is clear: “We want options that somebody could stay in for the rest of their life or until they want to take their assets out. So, if you start from that place, then I think helping your participants solve this issue or have tools available that will enable them to accomplish their goal and keep their assets in the plan and take advantage of low fees are all really good things.”

Looking ahead: nothing’s perfect. Providing guaranteed income, though, is the challenge. “As a plan sponsor, I’d like to be able to offer something that provides a guarantee,” the NeuGroup member said. But he, like other members, needs more information before making a decision.

- “Our investment committee is probably going to look at the solutions that are in the marketplace and determine if there’s anything that we want to add to the tools in the toolbox for our plan participants—realizing that there’s no single tool that’s going to be perfect.”

Dive in

Related

Article

Talking Shop: How to Respond to a New Rule on ESG Funds in 401(k) Plans?

Nov 3rd, 2020 • Views 16

Article

Talking Shop: How to Respond to a New Rule on ESG Funds in 401(k) Plans?

Nov 3rd, 2020 • Views 16